2024 is proving to be an eventful year.

Surely the US presidential elections in November carry most of the surprise potential, but a few other economic and war theaters are equally important for the global economy’s future.

Two major considerations spring to mind: geopolitical instability seems on the uptrend, while environmental volatility will not be easily overlooked going forward.

In the meanwhile, developed capital markets give us a picture of stability, if not optimism. Fundamentals in key economic sectors of major economies have never been stronger historically, while consumer confidence and expenditure are healthy. This fact pushed US equities and select European sectors to new historical heights. Bond returns are almost as high as they ever were over the past 153 years. Real estate prices have not collapsed anywhere – not even in China – due to higher cost of leverage. Corporate and household defaults have not increased. Mammoth debt piles are interpreted by governments and investors as just “being there”, rather than focusing on reduction.

The natural dissonance between what we think are dark clouds amassing on the horizon and the almost exuberance of today’s markets is not lost.

Global fundamentals

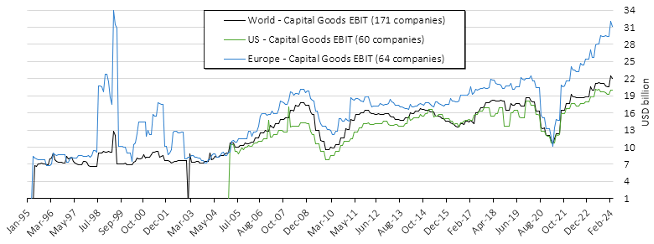

Capital goods are thought of the canary in the mine for any economy. They show what major orders of equipment and inventory are made by companies preparing for the future. In essence, are companies investing in expansion or are they tightening their belts?

Capital goods EBIT in the US, Europe and globally do not seem challenged so far. Yes, the pandemic dealt a blow to plans, but it appeared to be just a pause in a long positive earnings’ cycle, not the cane stroke that broke a camel’s back.

The most relevant move is that of European companies. The higher amount of capital goods orders might have be partially due to the shuffles in energy supply post-Ukraine’s invasion and to the gearing up of the armaments’ industry – see the Polish small arms and equipment manufacturers’ boom.

Earnings of capital goods companies

Perhaps with caution due to the boost of war-time industry, this is an overall reassuring trend. The development points towards economic expansion, not contraction.

The same trend extends to the US, which, safely out of a recession, seems to be experiencing renewed economic optimism this year.

Perhaps this optimism rests partially on the perennial quantitative easing the US is involved in.

Debt considerations

The US is without doubt the most sophisticated economy of our times.

The economic phase in which they find themselves today is that of growth being possible only through leverage.

While the initial plan might not have contemplated the current status quo, today we can safely assume there is no plan to repay the existing mount Everest of government treasury debt at any point in time. Nor is a reduction contemplated.

The only solution is keep printing dollars and distributing the existing and new debt stock among buyers.

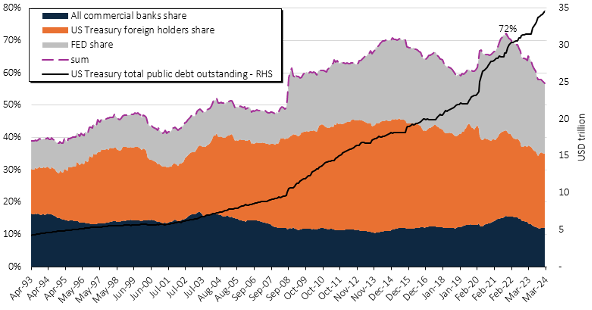

Who are the major buyers of US debt? Foreign countries have historically held the lion’s share, but the FED has taken on the driving seat post-GFC.

This balance has recently changed in that both the FED and foreign countries have been unloading US treasuries, the latter not being a good sign.

As a way to counterbalance this shift in buyers, the ISDA – a club of major global banks – proposed to the FED to (1) exclude US treasuries from the leverage ratio when calculating the exposure banks have to risky assets, and (2) that ISDA banks buy much more of US treasuries to cover for running buyers. This suggestion would make a fragile, concentrated and obsolescent banking system even more systemically important.

Owners of US treasuries

This is not a reassuring situation. The problem is the philosophical challenge to the US being the first “risk-free” reference.

It is tantamount to start doubting that gold is a haven in times of crisis, because it will always hold a certain value no matter what happens to the global economy.

The US administration answer to this challenge is to double down on (1) debt expansion, (2) currency printing and (3) making the banking system even more and concentrated.

While we might agree this is the only way forward, the US system might be overplaying its hand in an game where allies are starting to have doubts on US supremacy and competitors are joining forces to present a united front. We might not live to see a shift in global powers, but these moves do not look like short-term adjustments.

As of now, investors do not really have an alternative to investing in highly liquid USD-denominated assets, which most often are American businesses.

Capital markets

We mentioned before that the American economy is the most sophisticated of our times. This is because of technologic advancements.

As the final stage of economic development, technology holds the strongest potential for efficiency, productivity and sustainable competitive advantage.

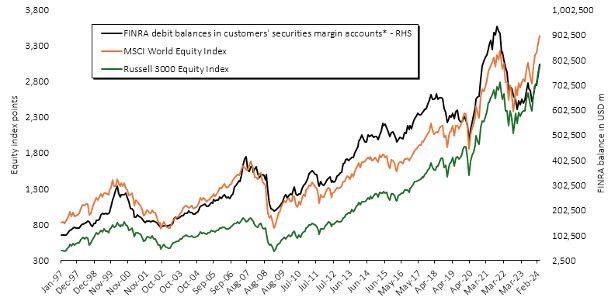

Since the deeps of 2022 and 2023, markets have now come back to previous historical heights. FINRA reports how the debt in margin accounts really drives US stock valuations, as seen below.

FINRA debt balance

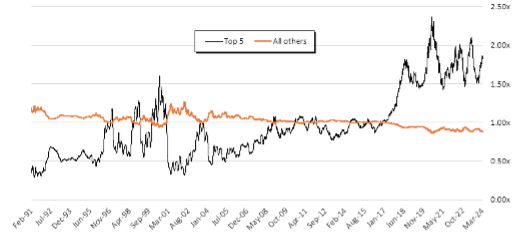

However, there seems to be caution from investors in this post-inflationary shock phase. The main evidence is a look at the S&P500’s top 5 companies’ share in market cap value versus their share of EBITDA – in essence, a comparison between market valuation and effective fundamental contribution to the index of the 500 largest US companies.

What emerges from this metric is that the top 5 most valuable companies of the S&P500 have traditionally held a healthy one-to-one ratio between market value share and EBITDA share, from January 1991 to January 2017. After that, the ratio spikes to historically unprecedented levels, to almost two-to-one. This ratio means that the market value share of the top 5 companies is double its EBITDA share of the overall index. Why? Tech names have gradually trickled into the top 20 of the S&P500 since the early nineties. By mid 2010s tech names in the top 20 took up the majority. Since 2017 the valuation of tech companies has simply sky-rocketed. We are now witnessing optimism mainly on these names, not on the overall S&P500.

So when commentators and news talk about recovering equity markets in developed economies they are missing the point that optimism is confined to the top 20 names of the S&P500. These names drag the entire index’s value upward, without the remaining companies experiencing similar investors’ enthusiasm.

Comparison between market cap and EBITDA shares

Note: market cap share: total market cap of top 5 names by market valuation over total market cap of the S&P500 index. EBITDA share: total aggregate EBITDA value of top 5 names by market valuation over total EBITDA of the S&P500 index.

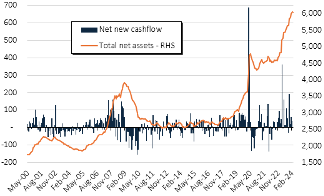

Another way of seeing the current skewedness of equity markets is through money market funds.

These funds are a parking spot in times of uncertainty, and surely become more comfy when base rates are high. Current US treasury returns are high in relative terms, which makes it difficult to

find better returns without assuming much higher risks to that of US govt debt.

| Net inflows and assets | Money market funds as % of total funds |

|

|

Source: Bloomberg, Index & Cie

In essence, investors are globally more parked in US treasury-linked short-term funds than invested in the wider equity market.

Within the equity market, investors chose to place their chips only on the largest names – in fact, tech names – of the US economy.

This is very different than seeing renewed and widespread optimism, and it shows caution is still predominant.

Chinese real estate

One last mention is reserved to the Chinese real estate market.

China and its organic challenges are instrumental to have an idea of the global economic flows of the future.

Any serious country goes through its major economic test in its first real estate crisis. Despite troubles began right after the shutdowns of the pandemic, China finds itself in the initial innings of this test.

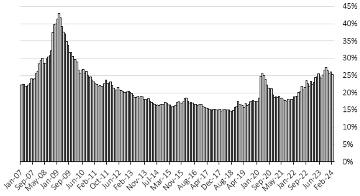

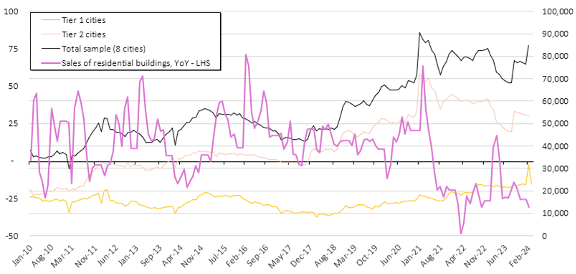

We have been observing two major trends: one where residential prices have either stalled or only lightly decreased in top tier 1 and 2 cities, another where the stock of sold residential units has dropped substantially.

Major residential prices and sales

It appears the major residential centers have not been hit with notable decreases. At the same time, sales have compressed substantially.

The situation points to Chinese residents pretty much sitting on their properties. The balance between mortgages and equity values has not become a problem yet, and there is little indication that will be allowed to happen by authorities. In turn, we expect major losses to be concentrated at a developer’s level, not on the wider population. The CCP has also announced a series of liquidity injections, which should contribute to stabilize prices in the medium term.

Conclusion

The clouds of recession in developed markets have dissipated, with developed economies in a healthy expansion mode.

American consumers spend away and corporations invest for the future. Similar situation in Europe, although the energy supply chain reorganization exposed some old balances that can be sustained no more. This reality leaves the flank of the Old Continent open to a decrease in competitiveness versus economies that have no problem and no sanction against cheap Russian energy.

Our search for quality names brings us almost inevitably to the US for the largest portion, but Europe is still home to some very strong players. Japan is not yet a source of global quality, not really because of their products and services – which we love – but because of management practices. Western activism in this respect should produce some positive results, although it is difficult to forecast when and how much on the basis that Japan has a millenary culture almost impenetrable by anything foreign.

Debt, geopolitical risks and wars will continue to maintain high the fear of inflation – through sustained oil prices – and we shall expect markets to continue moving along size more than quality.