Takeaway: China remains glued to its export business model, with an ever-present government support. The country is also experiencing the normalization typical of any large economic system that reached its limit to growth. Pivoting more significantly on domestic consumer demand remains a theory unverified by numbers. This is a potential internal headache at a time of rising geopolitical confrontation. It has resulted in the party adopting increasingly extreme measures to deal with malcontent around faults in its communistic social pact. We still like the long-term thesis, but we do not fault those who lost faith in it ever happening.

Another notable topic this year is China not really growing since pandemic times.

We believe this is really a story of economic cooling, natural to stable systems. After decades of commodity gobbling and frenetic infrastructural growth of the 90s and 2000s, China has not really succeeded in changing its cheap manufacturing, government-sustained model into an economy powered by its own consumer market. This market is indeed the second if not the first largest on the planet, but it is also entering a crucial phase of complexity typical of large economies.

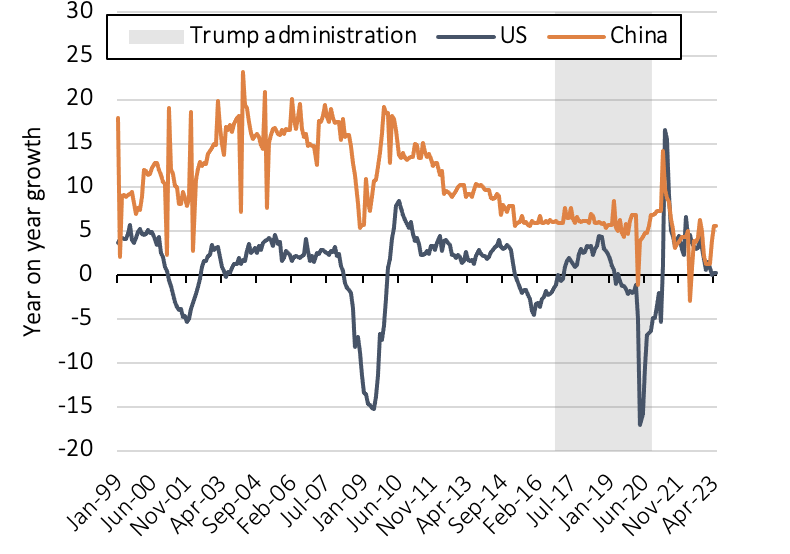

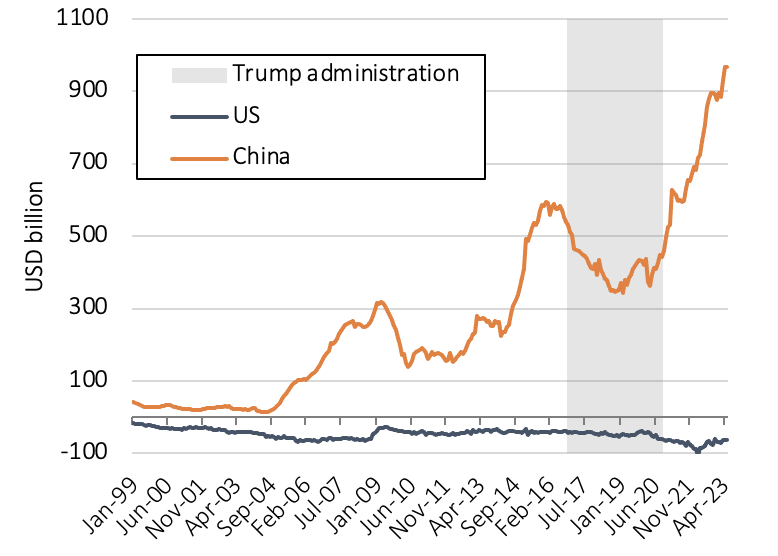

The labor market, trade balance and industrial production give it away. The comparison with the US is telling, specifically when trying to isolate the Trump administration effect – the one administration most antagonistic to Chinese business.

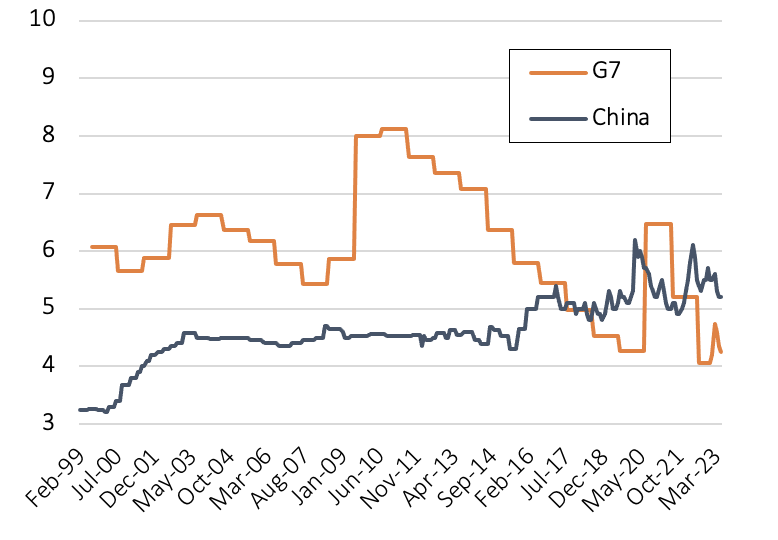

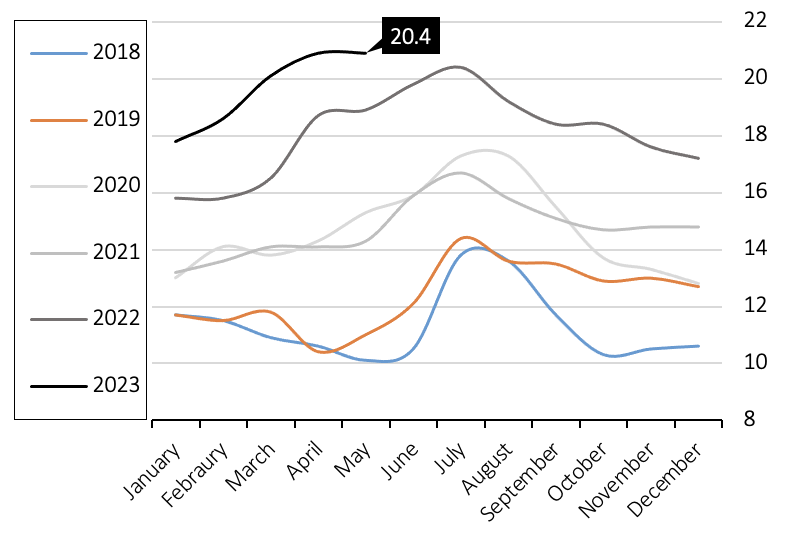

| Unemployment rates | Chinese urban unemployment rate among 16-24 year olds |

|

|

| Global trade balance | Industrial production |

|

|

|

The unemployment rate is rising among the general population, lately surpassing that of G7 countries. Youth unemployment is most worrying, with a peak of ~20% in May this year and in steady growth since 2018. This is a typical sign that a limit to economic growth has been reached in the internal job market. It is only inevitable.

From a trade balance perspective, it is evident global trade drives China’s economy. In comparison, the US have only worsened their net importer status, despite being energetically independent. The Trump administration did put a dent in China’s books, but only temporarily. Industrial production is perhaps the most compelling metric here: it is slowly approaching zero, and will naturally normalize in the same 5/-15% range the US traded around since the 1990s – that is, very low positive growth on average, with occasional and deep negative shocks. As a further confirmation, Chinese consumers are developing along the same lines of the Americans, with both household expenditure and retail sales year-on-year trends resembling each other.

Our view is that the oligarchy is now dealing with natural and serious limits to growth. Beginning with Mao Tse Tung, the communist party – composed of seven people commanding 97 million party members – locked themselves in a social pact with the country’s population that is increasingly harder to maintain. More extreme measures are becoming the norm, such as kidnapping CEOs of tech companies until they finally make public amends and hand over their capitalistic riches. Such interventions can only happen without setting off a revolution if the party ensures that everyone has a seat at the grand economic table.

It is clear that double digit growth in China is not repeatable. The next best thing is a strong improvement of internal consumer demand, one that reduces the national trade balance by importing more of foreign goods. The problem is that there is as much uncertainty on “when” this will happen as there is on “whether” this will happen at all.

As the fundamental angle remains inscrutable, perhaps history can provide some perspective on the market front.

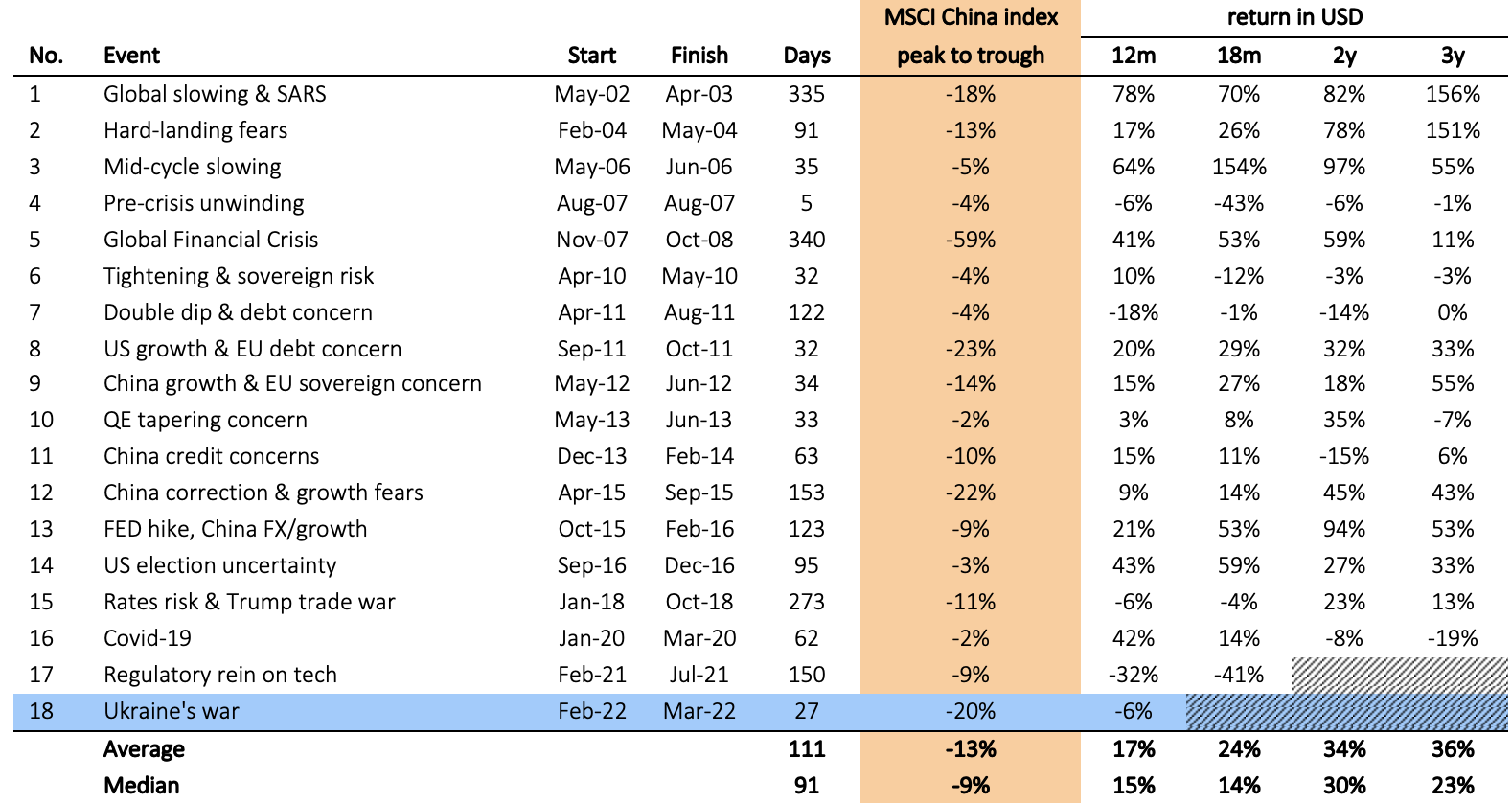

Chinese stock market crashes

This is the depiction of boom-bust cycles, mainly determined by foreign trust in the Chinese investment thesis.

The market recovery from 18 crashes has been quite fast, within 12 months from the trough on average. While encouraging, the current, persisting slump in valuation occurred only twice, during the 2007-2009 GFC and the global debt crisis of 2011. It is also quite possible that such prolonged slump is determined by a double whammy of reaching limits to growth and heightened geopolitical tension, which result in tariff and sanctions against Chinese exports. These two factors put the communist party in a delicate international position, the development of which we cannot map out.

Despite strong current headwinds, we remain positive on China’s economic strength in the long term. Yes, we cannot translate Western consumer habits on to a very culturally far civilization. Yes, the domestic market does not buy and probably need nearly as much Chinese manufacture as foreign buyers, which presents a problem of demand substitution. However, the sheer size of the internal market is indeed a unique feature of China. As much as the US is considered by any company to be the dream market for infinite expansion, China can become that market too.

We would love to see the much awaited business model shift toward internal consumption, but there is no trace of that so far. Any forecast is also futile. We do not fault those investors who threw in the towel, but history shows that flows will materialize fast when the economic signs improve.