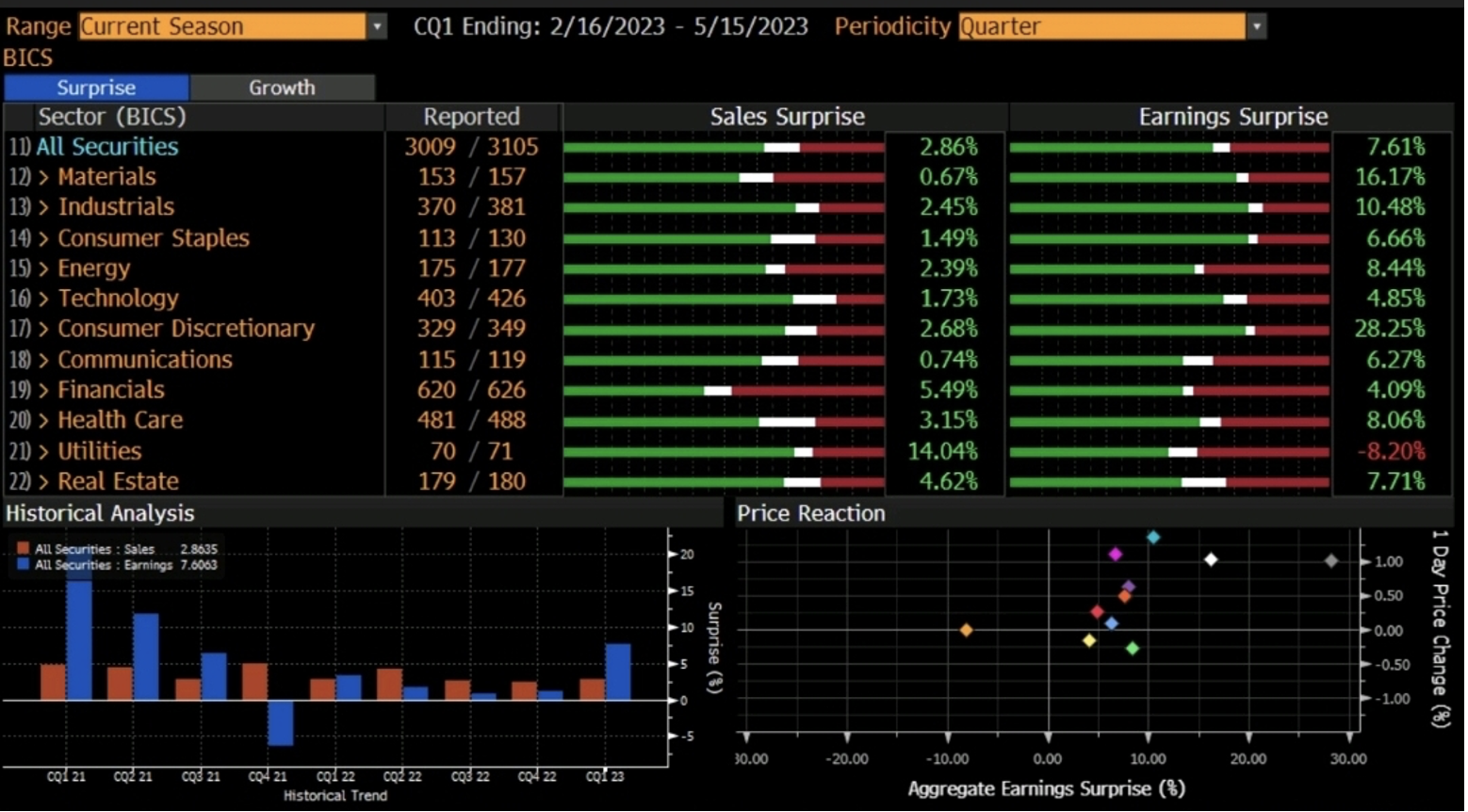

Takeaway: overall very positive last earnings season with tech and discretionary posting the largest surprises, very strong labor market, inflation somewhat moderating on the back of cooling energy prices, pretty solid household balance sheet with a continued expansion in leverage (mortgages). This is not the picture of an incoming recession, but could it be the unnatural calm before the storm?

We commented in our past letter how we are right in the middle of two important US macro shifts: the beginning of an earnings contraction cycle and the beginning of a US dollar depreciating cycle.

These two waves are likely to neutralize each other over time. As earnings cool due to a slowdown in consumption, a weaker US dollar brings in more dollars for the country’s exports, sustaining the GDP by way of higher corporate earnings. It is still difficult to quantify precisely the net result, but we believe the US economy will probably experience a soft landing, without much drama.

As of the last earnings season, results were pretty good in general and better than expected – see screenshot below. In particular, consumer discretionary earnings were 28% higher than expected, which is a strong indication of consumers’ health. Viewed in a historical sequence, Q1 2023 earnings rebounded strongly from a descending 2021 and a flat 2022.

A pro-recession investor would think “we are not there just yet”, but it is hard to see what other damages can higher rates do in an environment where defaults have not substantially risen – the previous graph shows the global default rate close to 1%, lower than the pre-pandemic one.

Last earnings season

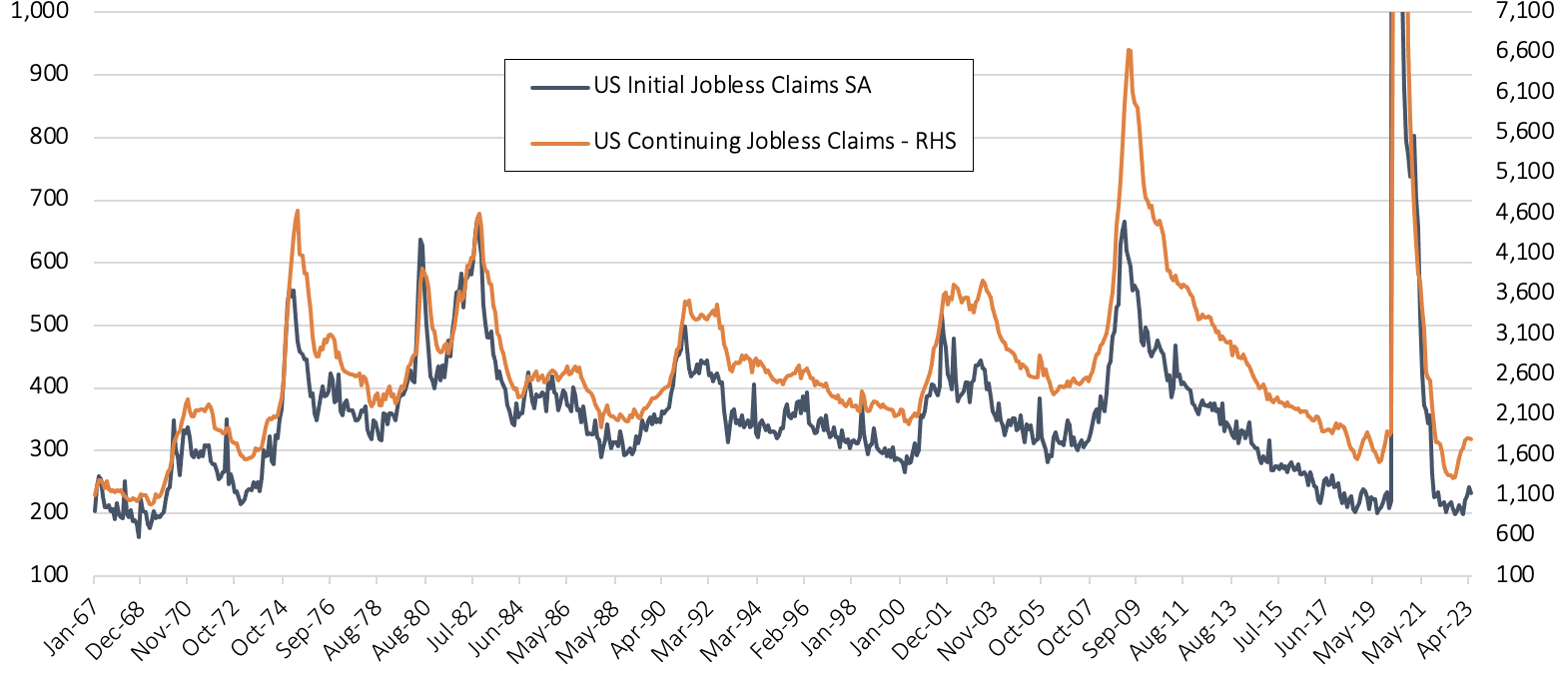

The job market too does not give signs of budging to any rate pressure.

US job market

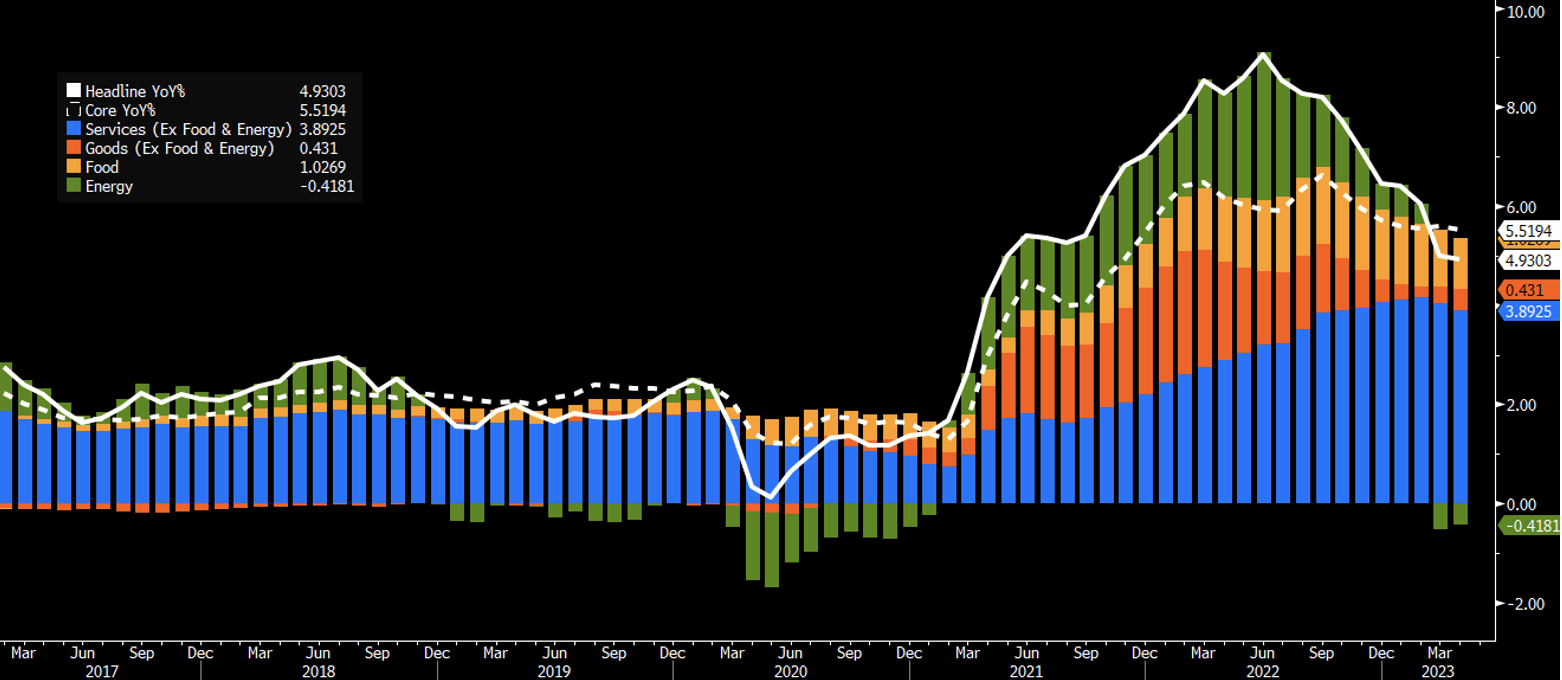

On the inflation front, reduced oil prices gave some respite to the overall trend, as seen in the composite graph below.

This development does not mean energy pressure on global inflation is over. It also does not mean this temporary drop will follow a similar pattern to 2020’s. It is of this week the announcement that OPEC is implementing a production cut to help sustain prices. Such measures have the obvious effect to keep inflation higher for longer, and to the detriment of event the oil exporting countries – which usually end up importing the inflation they helped keep high by way of imports.

Top-line contributors to US consumer inflation prices

In turn, such inflationary expectations are bound to be addressed by authorities. Last week the FED gave signs of pausing rate hikes in June. Markets took this announcement as the end of the rate increases. While this might be the case, we are not entirely convinced inflation is coming back to 2% any time soon, certainly not in 2023.

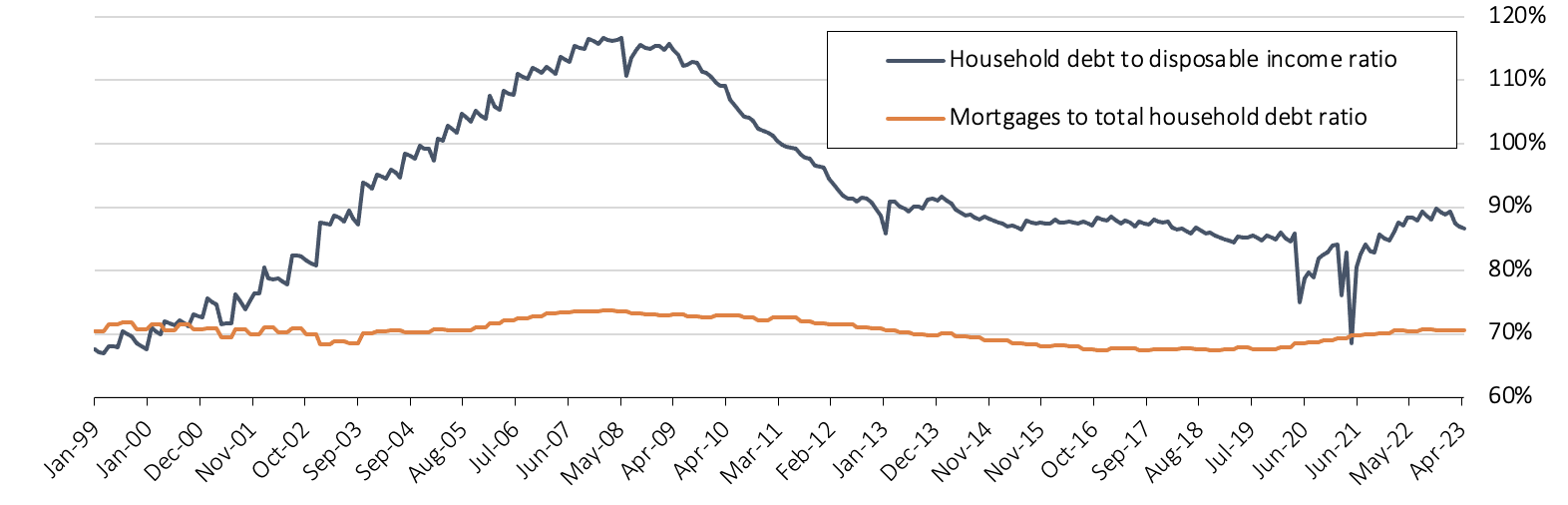

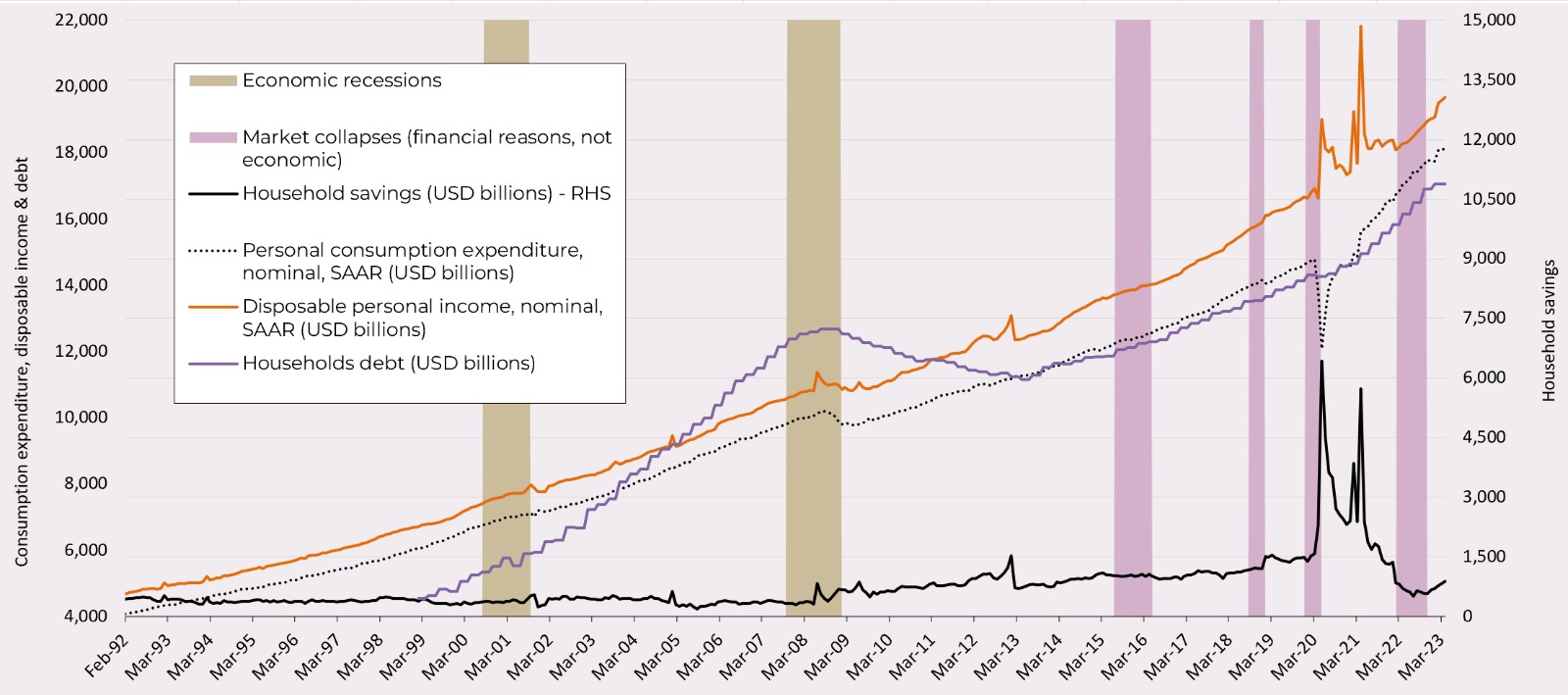

Among other measures, the US household balance sheet does not look unhealthy. the American population does not look dramatically different from other developed ones if one discounts that mortgages weight constantly 70% of the total household debt since 1999.

The US household balance sheet

In addition, the trend in household leverage signals expectations or the presence of a recession. The graph below shows that in 2022 and 2023 household leverage has expanded, not contracted. This is not a recessionary sign.

State of US household debt